On October 7, 2020, the Small Business Administration issued a new rule for PPP loan borrowers who received $50,000 or less in proceeds.

On October 7, 2020, the Small Business Administration issued a new rule for PPP loan borrowers who received $50,000 or less in proceeds.

That new rule says borrowers can receive full forgiveness of their loan regardless of changes in employee headcounts or pay rates. The only real requirements? Borrowers must make representations about how they handled their PPP loans. And borrowers must back up their spending with documentation.

Most PPP borrowers get to use the new simplified approach. And if you can use the simplified approach, because your loan amount equals $50,000 or less, you want to use it. And apply now.

We blogged about this last week. But then got lots of email questions asking about how one completes the form. Accordingly, this blog post provides a copy of the Appendix in our “Maximizing PPP Loan Forgiveness” ebook which steps readers through completing the application.

Completing the 3508S Application

The one-page 3508S forgiveness application (downloadable as a pdf here) requires about a minute to complete. You only need the original PPP loan paperwork (since it provides the loan date, number and amount.)

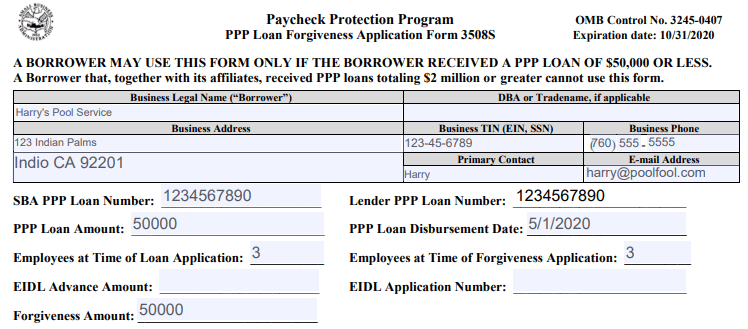

The figure below shows an example of the top part of the form which you use to provide contact information:

To complete this part of 3508S loan application, a borrower takes the following steps:

1. Identify the borrower.

Provide the business’ legal name, any “Doing Business As” or trade name, and then the address, the taxpayer identification number, and the contact information including a phone number, contact name, and email address.

2. Identify and describe the loan.

Provide the SBA PPP loan number (this number appears on the loan documents), and Lender PPP loan number, as well as the PPP loan amount and the PPP loan disbursement date.

3. Provide the number of employees at the time of the loan application and at the time of the forgiveness application.

Count employees as workers receiving W-2s. And note that a sole proprietor without employees enters zeros in both fields.

4. Describe any EIDL Advance.

If the borrower obtained an EIDL advance, provide the amount and the EIDL application number.

5. Specify the forgiveness amount requested.

If you correctly calculated the original PPP loan amount and spent those funds on forgivable costs, you should get full forgiveness.

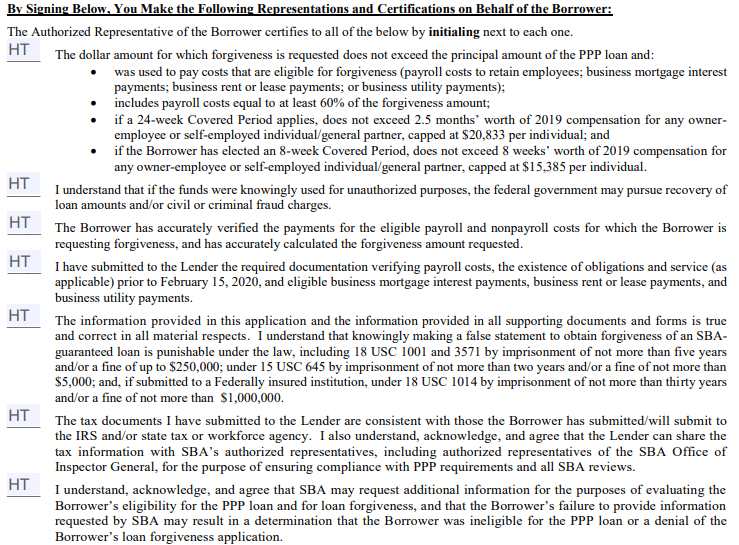

Representations and Certifications

You also need to make a series of representations and certifications. In a nutshell? You indicate you used the PPP loan proceeds correctly. So at least 60 percent for payroll costs. No more than $20,833 for each owner’s payroll. And then for any nonpayroll spending? Legitimate categories including rent on space or equipment, interest on business loans, and then utilities.

Tip: For nonpayroll spending, the borrower also needed to be obligated for the interest, rent or utilities prior to February 15, 2020.

The next image shows the part of the application that asks the borrower to make these representations and certifications: But note that all you need to do to complete this part of the PPP loan forgiveness application is initial each representation and certification.

For example, to indicate that you’re requesting the appropriate forgiveness amount, initial the first box. Then read and initial each of the other boxes. In the figure below, each representation and certification is initialed with the letters “HT.”

After initializing the representations and certifications, only two steps remain.

Signatures

The borrower needs to sign the forgiveness application using the signature block at the bottom of the form (see image below).

And then, second, the borrower assembles the documentation that proves the PPP loan money went for forgivable spending.

Note: The 3508Sform includes a second page (not shown) which asks a borrower to indicate whether the owner is a veteran and to report on the gender, race, and ethnicity of the owner. You don’t have to provide this information.

Documentation for Single Worker Sole Proprietor Situations

For roughly half of 3508S applications filed—those with just a working owner and no one else—the forgiveness application documentation should be incredibly easy to supply.

If a borrower operated a sole proprietorship and employed no W-2 workers, the forgiveness application only needs to include documentation showing the borrower paid out the loan to the proprietor.

For example, say a borrower’s 2019 Schedule C tax form shows the borrower earned $48,000 in 2019. This profit amount equates to monthly equivalent payroll of $4,000 because $48,000 divided by 12 months equals $4,000.

This borrower should have received a $10,000 PPP loan. The PPP loan formula multiplies the average monthly payroll by 2.5 to calculate the loan amount.

In this case, the borrower only needs to provide documentation showing that over the 24 weeks following receipt of the loan, it paid out $10,000 to the owner. For example, ten $1,000 checks paid to the proprietor work. So do ten $1,000 electronic remittances.

You get the idea. To document the $10,000 of spending, the forgiveness application includes cancelled checks or bank remittances or other documentation that shows $10,000 of payments.

Documentation in Complicated Situations

In more complicated situations, a borrower goes to more work to assemble the documentation.

But you want to keep four simplifying principles in mind. You want to

- Document enough forgivable spending to get full forgiveness. In other words, if you need $50,000 of forgiveness, you need $50,000 of documentation.

- Show at least 60 percent of the spending went toward payroll costs, including salaries, wages, state payroll taxes, group health insurance, and retirement benefits.

- Work from the easiest to gather documentation you can—which is probably any payroll reports prepared by a third-party payroll service.

- Document both the payment and the reason for a payment for nonpayroll costs. For example, if you want forgiveness for paying rent, you need both a check to the landlord (to show the rent payment) and the rental agreement (to show the reason).

And two bits of good news here.

First, borrowers should find it easy to accumulate enough spending to receive full forgiveness. The PPP loan formula provided borrowers with roughly ten weeks of payroll. Yet, a borrower can look at spending over 24 weeks.

Second, while a borrower received money to pay roughly 10 weeks of payroll through the PPP loan, the forgiveness formula allows a borrower to also get forgiveness for nonpayroll costs. The formula limits forgiveness for nonpayroll costs (rent, utilities and interest) to 40 percent of less of the loan.

Assembling Documentation for the 3508S Application

To document spending on payroll, a borrower needs documentation that provides both its cash compensation and non-cash compensation payments during the 24 week “spending window” that follows the borrower receiving the loan.

The 3508S instructions say this documentation might include for payroll spending:

- Bank account statements or third-party payroll service provider reports documenting the amount of cash compensation paid to employees.

- Tax forms (or equivalent third-party payroll service provider reports) for the periods that overlap with the Covered Period or the Alternative Payroll Covered Period:

- Payroll tax filings reported, or that will be reported, to the IRS (typically, Form 941); and

- State quarterly business and individual employee wage reporting and unemployment insurance tax filings reported, or that will be reported, to the relevant state.

- Payment receipts, cancelled checks, or account statements documenting the amount of any employer contributions to employee health insurance and retirement plans that the Borrower included in the forgiveness amount.

And then those same instructions say that for nonpayroll spending, the following documentation works to verify that an obligation or service existed before February 15, 2020 and that eligible payments were made:

- Business mortgage interest payments: Copy of lender amortization schedule and receipts or cancelled checks verifying eligible payments from the Covered Period; or lender account statements from February 2020 and the months of the Covered Period through one month after the end of the Covered Period verifying interest amounts and eligible payments.

- Business rent or lease payments: Copy of current lease agreement and receipts or cancelled checks verifying eligible payments from the Covered Period; or lessor account statements from February 2020 and from the Covered Period through one month after the end of the Covered Period verifying eligible payments.

- Business utility payments: Copy of invoices from February 2020 and those paid during the Covered Period and receipts, cancelled checks, or account statements verifying those eligible payments

The PPP program also requires a borrower to maintain, but not submit, additional information. Again, I’m going to quote the language the 3508S form instructions:

All records relating to the Borrower’s PPP loan, including documentation submitted with its PPP loan application, documentation supporting the Borrower’s certifications as to its eligibility for a PPP loan, documentation necessary to support the Borrower’s loan forgiveness application, and documentation demonstrating the Borrower’s material compliance with PPP requirements. The Borrower must retain all such documentation in its files for six years after the date the loan is forgiven or repaid in full, and permit authorized representatives of SBA, including representatives of its Office of Inspector General, to access such files upon request.

Submitting Form 3508S Forgiveness Application

To receive forgiveness, a borrower submits the completed 3508S loan forgiveness application (or an online equivalent) and any required documentation to the PPP lender.

The rules say the lender will “review the application and make a decision regarding loan forgiveness” and then within “60 days from receipt of a complete application” communicate that decision to SBA.

Assuming the lender decides the PPP borrower deserves forgiveness, as part of this decision to forgive, the lender then requests payment of the loan balance plus any accrued interest. The SBA then looks at the loan, presumably in most cases rubberstamps the lender’s forgiveness decision, and then remits “the appropriate forgiveness amount to the lender, plus any interest accrued through the date of payment, not later than 90 days after the lender issues its decision to SBA.”

For the hopefully small handful of cases where the forgiveness step gets bungled by the borrower, the borrower of course loses some or all loan forgiveness. In this unhappy event, a lender alerts the borrower about the loss or partial loss of forgiveness and “the borrower must begin paying principal and interest.”

One other wrinkle: If a borrower fails to apply for forgiveness within 10 months after the covered period ends, “the PPP loan is no longer deferred and the borrower must begin paying principal and interest.”

Thanks for taking the time to break down the process.

Hello. Can we also discuss this article: https://evergreensmallbusiness.com/ignoring-irs-8995-instructions-to-double-deduct-self-employed-health-insurance/

(Sorry to be off topic, but it was suggested on the contact page that jumping on an open article is the best way to discuss older articles.)

It has now been over 9 months since that article was published. Has there been any published cases since that time of conflict between a taxpayer and the IRS over this matter?

Secondarily, you say that your firm will “follow” the instructions but others may “ignore” them. Is it really about follow vs ignore? Isn’t it a matter of deciding if the deduction is “effectively” connected to a trade or business for the purpose of calculating QBI? Is there anything from the IRS that clearly disagrees with the logical in the article which says that it is not? (Other than a FAQ which carries no legal weight.)

Thank you in advance.

Hi Samuel, thanks for broaching this subject. I should do a deep dive on this, but take a peek at the flowchart for determining QBI here: https://www.irs.gov/instructions/i8995 … Look at box 10. Think about that a bit.

What I think? I think that says if some item is included in wages, it isn’t QBI.

Does this mean that someone who follows IRS notice 2008-1 (and so includes SE health insurance in box 1) doesn’t double deduct? I think so.

Woah, am I understanding that you have possibly changed your position?

Should the focus be on Box 10? AFAIK, we must consider “items of income, gain, deduction, and loss”. Is not a “deduction” one type of item and “income” another? Then if the item being discussed at hand is a “deduction” it is not “income” and therefore not “W-2 wages”. But maybe an item can be both?

My focus has been on Box 1. “Is the item effectively connected with the conduct of a trade or business within the U.S.?” My main focus is on “effectively” and also on an implied “for the purpose of calculating QBI, aka for the purpose of section 199A”. Then, as the article suggested, we have to decide what “effectively” means within the context of section 199A.

Quoting from the article, “Thus, for purposes of section 199A, deductions such as the deductible portion of the tax on self-employment income under section 164(f), the self-employed health insurance deduction under section 162(l), and the deduction for contributions to qualified retirement plans under section 404 are considered attributable to a trade or business to the extent that the individual’s GROSS INCOME FROM THE TRADE OR BUSINESS is taken into account in calculating the allowable deduction.” (emphasis mine).

As the article said, the deduction for an S-corp 2% owner-employee is connected to and limited by W-2 wages and NOT by gross income. This can be compared to and contrasted with a sole proprietor, for which it does make logical sense to include self-employed health insurance deduction in the QBI calc.

I want to also hit again on my first original question: Has there been any published cases of conflict between a taxpayer and the IRS over this matter?

(Sorry if this is a repeated comment. I wasn’t sure if previous submission went through.)

Woah, am I understanding that you have possibly changed your position?

Should the focus be on Box 10? AFAIK, we must consider “items of income, gain, deduction, and loss”. Is not a “deduction” one type of item and “income” another? Then if the item being discussed at hand is a “deduction” it is not “income” and therefore not “W-2 wages”. But maybe an item can be both?

My focus has been on Box 1. “Is the item effectively connected with the conduct of a trade or business within the U.S.?” My main focus is specifically on “effectively” and also on an implied “for the purpose of calculating QBI, aka for the purpose of section 199A”. Then, as the article suggested, we have to decide what “effectively” means within the context of section 199A.

Quoting from the article, “Thus, for purposes of section 199A, deductions such as the deductible portion of the tax on self-employment income under section 164(f), the self-employed health insurance deduction under section 162(l), and the deduction for contributions to qualified retirement plans under section 404 are considered attributable to a trade or business to the extent that the individual’s GROSS INCOME FROM THE TRADE OR BUSINESS is taken into account in calculating the allowable deduction.” (emphasis mine).

As the article said, the deduction for an S-corp 2% owner-employee is connected to and limited by W-2 wages and NOT to gross income. This can be compared and contrasted with a sole proprietor, for which it does make logical sense to include self-employed health insurance deduction in the QBI calc.

I always thought the double-deduction was nonsense. But we had and still have this language at the QBI FAQ:

And that seemed to say that you should double-deduct. In spite of the totally rational argument you make and which I agree with.

Before tax season, I read and reread the instructions. And concluded then that IRS thinks you should double-deduct. About as adventurous as I felt I could be was to point out that lots of people weren’t doing this. Even though one heard that IRS was saying “hey double deduct.”

Now I re-reread the 8995 instructions and look at that flowchart–and I’ve actually thought this for a while–and think that you can read them to say, “Hey, you should deduct.” But at the same time, if they’re in the wages, aren’t they already deducted?

> Now I re-read the 8995 instructions and look at that flowchart… and think that you can read them to say, “Hey, you should deduct.”

But does the the flowchart actually say “Hey, you should deduct” to *everyone* that takes the deduction? Or only to those for which the deduction is “effectively” connected to a trade or business for the specific purpose of calculating QBI?

I’d love your directly-stated opinion on my viewpoint that it hinges entirely on the word “effectively” and where else can we go to define “effectively” other than the regs you pointed out?

Is there *anything* at all other than the FAQ to counter that?

I’m not even 100% convinced the FAQ even says, unequivocally, that it should be double-deducted. The question in the FAQ is “Do I have to also include this deduction when calculating my QBI from the S-Corporation?”. Am I wrong in thinking that I’m “calculating my QBI from the S-Corporation” only when I’m calculating the K-1? When I’m doing my 1040, I’m calculating my personal QBI based on my personal items of “income, gain, deduction, and loss” which is separate from “my QBI from the S-Corporation”. When I’m calculating the K-1, the wages utilized for my SEHI reduces the QBI and because it reduces the QBI on the K-1, it ALSO has reduced my personal QBI. So this does in fact “result in QBI being reduced at both the entity and the shareholder level”. It seems to me that people are only assuming that the answer implies a double deduction because of their assumption of what the original question is trying to get at. If we read it directly at face value without assumptions, then perhaps it doesn’t necessarily say what so many people think it says.

So after we print the form and fill it out correctly where do we send it? Or where should we take it once done filling it out?

You sent the forgiveness application to your bank–or you fill out an equivalent online form what works the same way.

Hi where do we send the application mail or email plz let ne know thanks

You will send the forgiveness application to the bank who provided you with the PPP loan. Or, you may fill out an online version of the application.

i am behinf my mortgage .8 months i need help

Very sorry Richard. Unfortunately, the PPP program isn’t connected to a business owner’s ability to pay or not pay their mortgage. It only provides money to pay the owner and employees wages and then some overhead expenses.

If I turned my business into a mobile barbershop in stead of continue renting a building or paying weekly chair. Do I need to show payment for 2007 Dodge Sprinter.. Showing what I spent the money on.

I don’t understand your question. Sorry. I don’t think however that you can buy a sprinter during the covered period, call it rent, and get forgiveness.

Good and fine

Sir, my husband and I are one of many small residential rental and other type of family companies who were apparently too afraid to apply for the ppp loan since we are already too strapped with our bills to consider adding another payment should ours not be forgiven. We applied and received the $1,000.00 each EIDL which helped. Have you heard anything about this loan forgiveness program returning for families like us? TY

I don’t think you get forgiveness for EIDL loans. Sorry.

Hello, I’m self employed and I profited $1,800 a month in 2019. My PPP was $4,500 then a month later PPP deposited another $10k and called it adjustment.

My rent & utilities are $3k in total a month. I was off for 12 weeks, then back to work again, took me another 12 weeks to start profiting.

How do I get my rent and utilities of $9K forgiven (I suppose partially) since they are way more than 40% of the entire PPP I was awarded?

Thank you

If you’re 2019 Schedule C profit was $1800 a month, you were supposed to get a $4500 PPP loan and that’s what you can get forgiveness for. I think the other $10K is EIDL money. And you can’t get forgiveness for that. (But ask the bank.) BTW, you want to use the $4500 of PPP for paying Ameer the proprietor. That then becomes tax free income.

Thank you.

I used the whole $4,500 to pay me ‘Ameer’.

I just read on the SBA page that The $10,000 is an EIDL Advance and it is completely and separately forgivable provided I used it on the business and not on the same items I used the $4,500.

The EIDL advance will reduce the forgivable portion of PPP, if you received $10k, then the $4500 won’t be forgiven.

I applied for the PPP and received the SBA EIDL. Why is the EIDL not forgivable as the PPP?

It was the PPP loan that includes a forgiveness provision. EIDLs work differently.

Thank you Stephen. Is there not anything one can do to get the the EIDL forgiven?

Thank you Stephen. Are there any options available to have the EIDL forgiven?

The top right hand corner of the form 3508S says that it has an “Expiration date: 10/31/2020.”What exactly does that mean? Does it mean that no one can utilize this form after 10-31-2020? So the Big G provides a form that only has a useable lifespan of 25 days?

Ignore the expiration date. That’s basically a typo or error as SBA has now officially acknowledged.

Stephen, have purchased many of your books and appreciate all of the information that you post regarding various topics. I have a situation where a client completed their own application and included sub-contractors in their original employee count. Now they are completing the forgiveness application and realize those should not have been included. The original 11 employees are still employed but 20 employees were listed on original application. Is there any guidance you are aware of when there is an incorrect amount originally reported? Might this just end up being a reduction of 9 employees and a portion of the loan not forgiven? Open to any suggestions. Thank you.

I think what happens is, that extra money the borrower received due to the PPP loan amount error, they don’t get forgiveness for.

For example, they should have borrowed (say) $100K based on 11 employees but because they misclassified contractors, they got $200K based on a miscount f 20 employees. When they go to calculate forgiveness, they’ll make calculations based on the 11 employees. Probably but only roughly that’ll mean they get forgiveness for the payroll of the 11 employees and $100K.

I’m not sure there’s guidance on this issue, but it would seem to be keeping with the spirit of the statute to return the excess amount.

I received my loan directly from the SBA…no other lending institution was involved. I am Self-Employed. Can I request Loan Forgiveness? If so…how do I submit the Form 3508S or EZ to the SBA?

Hmmm. I don’t understand that. Sorry. Because the SBA guarantees loans (so lenders will lend). And then in case of PPP, the SBA pays off the loan if the borrower follows certain rules about spending the PPP loan proceeds.