I want to talk about sole proprietor PPP loan applications.

I want to talk about sole proprietor PPP loan applications.

More specifically, about PPP loans for sole proprietors who don’t employ other workers as W-2 employees.

But some backstory…

Why this Post for Sole Proprietors

Over the last few weeks, a nice fellow has been painting my house. Great painter. The house, when he’s done, will never have looked better.

Which doesn’t have anything to do with your sole proprietorship or with PPP loans. Except for one thing. In talking with the painter, I learned that he had failed to obtain a PPP loan earlier in the year. Though he clearly deserved one…

I also learned that his brother, another self-employed painter, failed to get a PPP loan.

And then, no surprise, their dad who is also a painter? Yeah, he failed to get a PPP loan, too.

Partly, the guys didn’t realize PPP loans amount to free money.

But mostly the PPP loan application program proved too complicated and confusing. Which turns out to have been true for too many small business owners.

Accordingly, I’m going to explain here how to fill out the PPP application for a sole proprietor without W-2 employees. The actual work of completing the application takes, no kidding, about two minutes.

But before I get to that, let me explain why I’m getting all pushy and nervous (on your behalf) about this.

Why Sole Proprietors Want to Get Ready to Apply for a PPP Loan

The actual PPP program ended August 8, 2020. A business owner can’t therefore apply for a PPP loan right now.

But business owners need to be ready to apply. Why? Proposed legislation from Senator Marco Rubio may restart the PPP briefly sometime after Congress returns after the Labor Day weekend.

And then, the other key thing to know. If Congress does restart the PPP, the pool of money may get drained fast.

Note: The new PPP loan “phase,” if it is based on Senator Rubio’s bill, will allow some borrowers get a second draw PPP loan. That will use up money fast. And it will also allow some earlier PPP borrowers to increase their earlier PPP loan balance. That will use up money fast.

You can understand why I’m nervous on your behalf… You want to plan ahead. You probably need to move fast.

Applying for a Sole Proprietor PPP Loan

To apply for a sole proprietor PPP loan, you want to have your 2019 1040 tax return done.

Why? Because the Schedule C page of your tax return sets the loan amount. See the fragment of a Schedule C shown below? That bottom line $48,000? That sets your loan amount if you’re a sole proprietor without employees.

The actual loan amount formula? You get 2.5 months of your average monthly Schedule C profits.

So, if you made $48,000 in 2019, that means you averaged $4,000 a month. I calculate this amount by taking $48,000 and dividing that value by 12 months.

And then the loan amount? Well, 2.5 times $4,000. So $10,000. That’s it. That’s the number for a sole proprietor without employees who made $48,000 in 2019.

Applying for PPP Loan

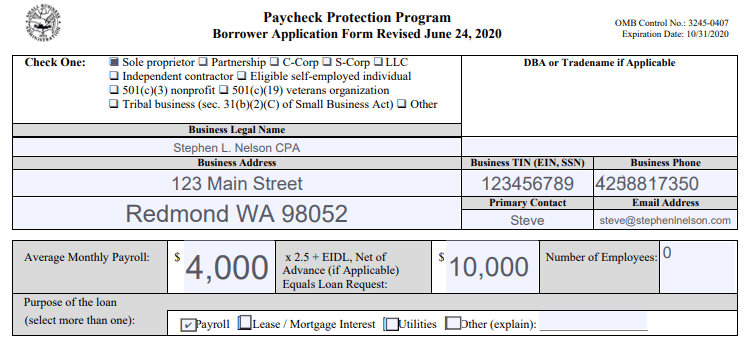

Once you have your “number,” you grab a copy of the PPP Loan application from either the Treasury.gov or the SBA website.

The top part of the form, shown below, provides the fields you fill in. Notice that you provide your name and address and your taxpayer identification number. And then you provide the monthly payroll amount and calculate the appropriate loan amount. And that’s the only hard part…

You will provide a bit of additional information in order to apply. For example, you will identify the sole proprietor by filling in a few blanks:

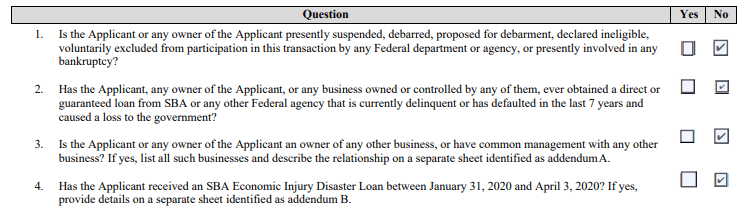

And then you go through some checklists.

The first checklist, for example, asks you indicate whether you (you’re the applicant) have or haven’t done some stuff:

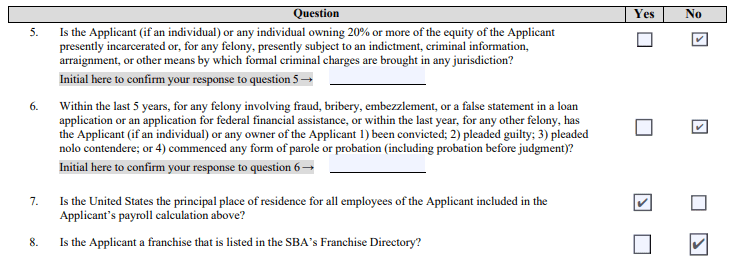

The second checklist, shown below, asks if you’ve been in trouble with the law, whether the business’s employees (this just means you) reside in the US, and whether you’re a franchise operator:

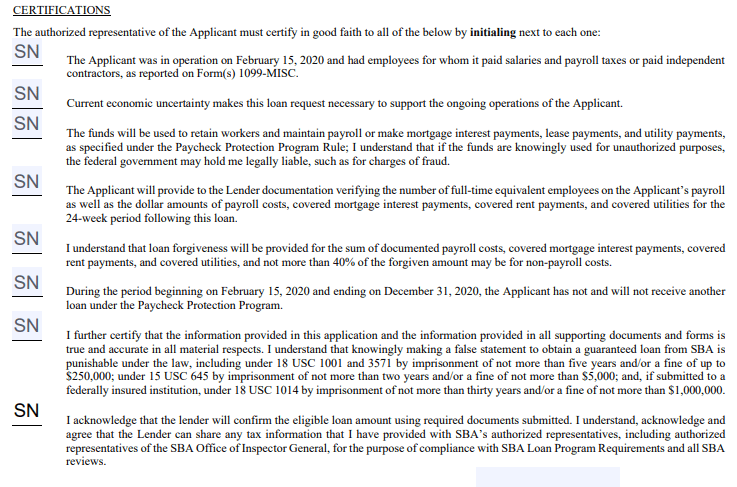

Finally, a last checklist asks you to initial a small list of “certifications.” The first certification, for example? That you were “in operation” on February 15, 2020. The fragment below shows this part of the application:

But that is it. The only other thing you do is sign and date the application.

Like I said, for a sole proprietor without employees? This PPP application should be a snap. Two minutes or less. Once you have your Schedule C printed out or on the screen in front of you.

Closing Thoughts

My suggestion? Grab the application. Get it filled out (using the information from your Schedule C form.)

Then talk with your regular bank about whether they will restart their PPP lending program if Congress restarts the program.

If they won’t? Talk to any other local banks you know. The smaller community banks may be your best bet.

And then be ready to apply if Rubio’s bill passes.

P.S. Very possibly, the bank won’t actually have you fill out the official Small Business Administration application form. PPP lenders can create online versions you fill out using a computer. You should complete the actual PPP application, however, since it steps you through the calculations and collecting the needed bits of information.

I received one but this is great information. Ray tho understand….thank you!

How about a professional Landlord who has a lot of apartments. All income is reported on Schedule E. But he has all properties under different LLC’s and another LLC manages the rentals, collects all rent and pays out to him monthly the profits.

Even if they would accept Schedule E income, after depreciation Schedule E might show zero taxable income even if the positive cash flow allowed the Landlord to take home over $100k/year.

No, sorry, that doesn’t work. You need something operating an active trade or business. Something that’s causing the business owner to pay self-employment taxes.

Thanks for your reply! I managed to get a PPP loan for my rental business, but I might have trouble getting it forgiven because they’re asking for payroll, but paying myself from the LLC, I don’t file any payroll forms.

My CPA offered a resolution to your problem with payroll. Write yourself a paper check from your business account to yourself. Write payroll in the memo in the amount forgivable for payroll expenses. This allows a paper trail for PPP forgiveness.

I think/agree a sole proprietor needs to make a payment to him or herself. That’s in the instructions.

Very simple and clear information about pop loan.

Thanks again for the explanation.

What about applying from the Kabbage app?

I think the fintech companies (like Kabbage) have worked really well for many small business borrowers. BTW I have no affiliation with Kabbage…

Kabbage is a huge ripoff..they approved 1000s of loans for small businesses..then after loan docs were signed they began requesting the same docs over & over again..only to send emails saying that the loan couldnt move forward because they couldnt verify identity..really?? Out of 20 identifying documents..they couldnt verify identity?? They telllyou that your loanhas been cancelled..only for you to find out later that it wasnt cancelled and they are charging you interst on it..They lie and give excuse after excuse…they are have being investigated for mishandling so many loans & a class action lawsuit will be coming soon …if youre in need of this loanto save your business..dont use Kabbage..it will only guarentee that youll loseyourbusiness

I experience the same thing with Kabbage they sent me a email congratulations. Me for being approve then say I need to do c usign but never received email than they say my loan was cancel because the 20 days have expire

OK, so that sucks. And good for people to know this process is fraught with pitfalls. But don’t give up. Try again when/if they restart the program.

You are right they told me they could not identify me.they say I need to verify my identity I sent all the documents needed I’m a legitimate business and I never got the funding. I know folks who don’t even have a business and did fraud and got money. All the people that was honest on the application did not get money

I agree and can attest first hand to the Kabbage RIP-OFF! They should never be allowed to do PPP loan apps ever again.

Thank u very much

What do you do if you haven’t been in business long enough to have a schedule C? Started my business in December of 2019.

You qualify. The PPP formula looks at January and February 2019 for PPP loan. And at 2020 for second draw loan.

Great article. Informative and easy reading.

sorry is almost impossible to understand all of this,

can you let me know if Rubio passes the law??

I am a sole prorpietor aos a small property in brooklyn, i do not give payroll, as I don’t have anybody, I just pay myself from the money I received,

I ahve beeb having terrible loss in the last seven months. I might not be able to pay the mortage on my propery, how can i apply for a lona?? Ior grant i alrady lost about more thna 60 dollars, who is going to give me some of my moeny???

and whom can i ask?? many thanks

Oh Maria, so sorry… but if you’re a property owner (so like rentals) the PPP doesn’t work for you. It’s not for real estate investors. It’s for active trades or businesses. Very sorry. 🙁

Too bad they don’t help sole proprietors that show a loss. There are many out there that can use legitimate deductions to show a loss.

True I agree. My schedule C on that line is zero but I still need the funds bad.

Hi

Whats the minimum credit score do I need to qualify ?

Bad credit won’t matter. You want to apply if PPP restarts.

I’m sorry but credit score matters. I was denied because my score was low. Personal score should be not allowed. It should be D&B where I have a great business score. I did not receive the EILD Or PPP!

I believe you. But the statute said the credit score shouldn’t matter except for a few special cases (like defaulting on a prior SBA loan).

Thank you

If you got a ppp loan once can you apply again

You may be able to apply for a second draw loan or a loan increase. See here https://evergreensmallbusiness.com/ppp-second-draw-loans/ and here https://evergreensmallbusiness.com/ppp-loan-amount-increases/

What if we declared a loss in 2019, but only after depreciation–prior to facility and equipment depreciation we were a little bit on the positive side. Is it worth admitting to apply, or does that situation exclude us from applying?

You don’t get much PPP loan if you showed only a really tiny amount of income. And you don’t get any PPP loan if you showed a loss.

I maybe shouldn’t say this, but probably whoever prepared the tax return should have thought of trying to legitimately slow down the depreciation deductions in order to get a Schedule C profit that produced a PPP loan. For example, it may have been without Section 179 depreciation or without bonus depreciation the business showed a profit.

P.S. Remember, too, that the PPP loan for a sole proprietor looks both at the proprietor’s income AND the W-2 wages paid to employees. So even if the owner didn’t make money, the business may be able to get a PPP loan that covers some payroll for W-2 employees.

I applied and received a PPP loan submitting ONLY my part time employee’s W 2 wages. It didn’t cross my mind to include my net income. Can I reapply?

Maybe! You would apply for a PPP loan amount increase (because you probably borrowed too little the first time). More info here: https://evergreensmallbusiness.com/ppp-loan-amount-increases/

I was unsuccessful twice trying getting a ppp loan.im a sole proprietor Independent contractor.

Ok, so sorry to say the predictable thing, but you want to try again if the program restarts. Maybe with a different lender. Maybe with a fintech company like Kabbage or Paypal or Intuit.

What about credit history or bankruptcy

A bad credit history or a bankruptcy doesn’t disqualify you. You do probably (possibly?) get disqualified if you’ve defaulted on an SBA loan before.

What if u had a loss in 2019?

I think that precludes you (unless you’re a farmer or rancher).

Steve how will u pay DA loan back

You don’t pay the “loan” back. You use the money for the stuff Congress wanted to subsidize: payroll, rent, utilities, owner compensation replacement, etc. And the SBA forgives the loan.

What about farmers who are disabled like me who showed a loss on sch. F. The main reason was to get back my 401k tax that was withheld.

Hi Kenneth, you want to see if Rubio’s bill (the one we’re talking about here) passes… and then if that’s case, you want to recalculate the PPP loan amount using the new rule for farmers and ranchers. See here for details: https://evergreensmallbusiness.com/ppp-loan-amount-increases/

I’m interested in the PPP loan.

Hi Vincent, we’ve got a bunch of articles here at the blog. Many are written for CPAs. But you might be able to learn more from these: https://evergreensmallbusiness.com/?s=PPP

Hi, This article is very helpful for me, thanks a lot. I have some questions about 2nd ppp loan.

I’m independent contractor(small delivery business job), and reported tax using 1099. And the company deposit to my account directly every month, so I don’t have any documents (invoices, pay stubs..). My question is, if 2nd ppp will ask ‘decrease income than before ‘ and then how to show that? I just have tax report as official documents. Could you please give me a good idea? I need a 2nd ppp loan. Please share your wisdom. Thank you.

Here’s my blog post on PPP second draw loans: https://evergreensmallbusiness.com/ppp-second-draw-loans/

I applied for the. PPP. But when they used my schedule C. I only received 1400 dollars. Bc of my deductions. My bottom line takes away. Some is better than none. So i lost out on the PPP. No one listens . they Did Not go by my payroll.

If you have employees, you can get PPP money for their wages. For example, if you made roughly $6000 in Schedule C profits (because of the deductions), that means you averaged $500 a month and so get $1250 in PPP loan money for that. But if you also had (say) an employee who earned $2,000 a month, the PPP formula will provide you with another $5,000 for that.

In other words, even for a sole proprietor, the PPP loan formula looks at sole proprietor profits PLUS W-2 employee wages.

If you got short-changed, you should be able to get a bump in your original PPP loan if the new law passes. This other blog post explains: https://evergreensmallbusiness.com/ppp-loan-amount-increases/

We have farming land but due to recent corona virus crisis the lender took it back and put on auction now , need help to retain this property .

Regards

Mehmood Shauket

Oh man, my heart breaks for you guys. And in the new bill, they provide special help for farmers and ranchers… See here: https://evergreensmallbusiness.com/ppp-loan-amount-increases/

I would say you guys pay close attention to the new PPP bill (so Rubio’s bill) and then try to get a PPP loan based on the new farmer and rancher rules… and then you see if with that money you can restart your farm.

Good luck!

How about individual business owners with no employees that file using 1120S or Partnership Returns?

If a business operates as an S corporation, it needs employees to create the payroll that plugs into the PPP loan amount formula. So no employees with payroll, no PPP loan.

For partnerships, the partnership (not the partner) applies and uses the partner self-employment earnings reported on the partnership K-1s that go to partners as the payroll amount. This is a little bit more complicated then the sole proprietorship situation. But conceptually, the process woks the same way.

I applied in July, I am a Realtor and they asked me for Organizational documents. I emailed back and asked what that was and they were responding vaguely not explaining what it was. I only had the schedule C for 2019. I had already uploaded that.

After a few weeks I received an email from Kabbage saying my loan expired for not sending in what they required and I was waiting for a response the whole time. SMH.

Hmmm. Organizational documents would maybe mean LLC articles of formation? Or articles of incorporation? Maybe a business license if required?

The fintech companies (like Kabbage) because they’re doing everything online require you to provide enough paperwork that you can substantiate you are a real person. Maybe they just needed some more of that stuff…

I think you should try again if you had a Schedule C in 2019 that showed a profit.

?

? 🙂

What if i have just started my own buisness and naturally has been put ” on hold” due to the public health emergency covid -19?

Would that qualify me to apply for one of these buisness loans? If so roughly how much money should I ask for? Idealy I would like to believe that I would be making x amount of dollars, yet again I have been hindered in doing so.

I also have been self employed and done construstion clean ups, renovations, house cleaning jobs …. Wuthout a LLC does that qualify me for one of these loans?

I don’t think so. You needed to be operating on February 15, 2020. Sorry.

Hi, I was denied the loan and they said the reason was my credit. I don’t understand …

Hmmm. That shouldn’t matter. Maybe try a different lender if the program restarts?

BTW, some of the banks were TERRIBLE in the way they handled this. If the walls of our CPA firm offices could talk? Oh gosh, the PPP stories they would tell.

But let’s leave it at this. We say situations where big banks (er, the biggests) told long-time customers with impeccable histories that they weren’t good enough to get a loan. Go figure…

I was rejected straight from SBA for credit weak

I too was not given the loan due to credit and I applied directly with sba. If it should not matter why did it and how do I appeal it

So that’s a good point. You don’t apply to the SBA. You apply to an SBA lender that does PPP loans.

In your case, Melanie, I would try again if/when they restart the PPP. And maybe work with a local bank. We’re seeing some real criticism of Kabbage. I don’t have any first hand knowledge of that. But frustrations and disappointment with ANY lender don’t surprise me. (Most of my experience was with the really large banks… and those guys made a lot of people unhappy too.)

This idea–and remember I’m on your side if you’re trying to borrow–just focus on getting the loan. That’s the prize to keep your eye on…

PPP,

Thank you for taking the time to share so much helpful information! I am a small business owner as well, who was turned down for ppp loan. And it was due to me not understanding what I was actually filling out.

I Have taken your advice and prepared myself for the anticipated Opportunity to file once again!

Thanks to you I AM READY!

MIMS Services, LLC

Indianapolis, In

Excellent Angela! It’s taking care of these sorts of tasks and opportunities that’ll make all the difference! 🙂

Thank you for this information. I just started my sole proprietor company May 22,2020. So i don’t have 1 year in yet to do the calculations. But great article

What if you started your business this year and dont have a 1040 but you filed taxes (W2) in 2019?

You needed to be in business on February 15, 2020. And then you need profit in 2020. Other readers have asked this question and I’ve answered them so scroll around the comments?

In the last questions… …the certifications SN questions

It asks about full time employees where or when I have none…I run it by myself…. in the SN questions they talk allot

about employees …. why? I thought this was all about

being a sole proprietorship….It gets very confusing at that point.

Good question. And I just reread the certifications with your comment in mind. You’re absolutely right. It is DARN confusing.

You can consider yourself (so the proprietor) as an employee. You absolutely are eligible.

As a grub hub driver can one apply for the loan

If you made Schedule C profit, yes.

We have tried over and over again to apply for a PPP loan . It’s very difficult to get approved. Go figure!!!

Sorry! I would try again if the program restarts. And get in line early. And maybe try both a local community bank and then one of the “fintech” or “financial technology” companies like PayPal, Kabbage, etc. Intuit may be doing them too.

Good information hopefully I’ll get to use what is very much needed. Clarification is what I need as a new business owner.

God bless America in helping g with these programs and President Trump’s creative and nonstop ideas.

I made $72,085 in 2019 and only recieved $8,500. When you divide $72,085 by 12 it comes out to $6,007 per month which comes out to $15,017.50. Is that what I should have received? Does it matter what title a person uses like self employed, sole proprietor or independent contractor because i was only able to apply as self employed?

So if your Schedule C bottom line (like in the blog post) showed basically $72,000, that equates to $6,000 in profit each month. And, so, you’re right. You would/should have gotten a $15,000-ish PPP loan.

If the bank or your PPP application calculated wrong and this new PPP loan program starts, you should be able to get a PPP loan amount increase to “fix” the error. More details here: https://evergreensmallbusiness.com/ppp-loan-amount-increases/

I started my business this year so I don’t qualify, but I wanted to note that you are an awesome person for posting this.

🙂

Wow! This was very informative can you email this to me

thank you so much

Wonder if I recieved a 1,too. I dont know I’d that was PpL or the grant

Thank you l really appreciate this .

Thanks for the info. ? If am S.P. of a small business (Delivery)and working full time with another company and was laid off , am I qualified to apply for ppp under my business and also apply for disaster insurance benefit (unemployment) because of my layoff. Please appreciate an answer.

Thanks

Good question Raymond. And I don’t know the answer. I would think this depends on the state’s unemployment insurance rules. You may be able to get a PPP loan though… so do continue your research. (And sorry I can’t give you much of an answer.)

Thank you. There so many small businesses owners who desperately needed this simplified breakdown.

I read through this blog. There is good information here. But I’m an LLC and had no articles until after February. However I have claimed loss on my taxes for my small business last year for items I purchased and depreciation. Can I apply too or is this sole proprietor only? Or did just confuse everything’?

An LLC owned by one owner is ignored. Tax law also uses the word “disregarded.” I.e., a single owner (or single member) LLC is disregarded for tax accounting purposes.

What that means in your case, probably, is that the LLC doesn’t affect ANYTHING! 🙂 So you just have a sole proprietorship. And then you get into the question of whether or not you had profits in 2019… those profits “set” the potential PPP loan amount.

It sounds like you didn’t have profits but did operate. So that unfortunately means you don’t get a PPP loan. Sorry.

BTW, different rules apply if you started your business in 2020. (As noted in other comments.)

Tremendous article. Finally a CPA who knows how to communicate simply and effectively. One question: Can a sole proprietor who already received a ppp loan get a second one if this new legislation passes?

Maybe… you would either need to be especially hard hit and qualify for a second draw loan. Or you’d need to be someone who didn’t get your full PPP loan amount the first time and so can take another bite at the apple.

More info here: https://evergreensmallbusiness.com/ppp-loan-amount-increases/ and here: https://evergreensmallbusiness.com/ppp-second-draw-loans/

You will get a loan if you have pretty books and you could get a loan with out it from a. Bank that knows you .

The biggest issues with sole proprietary on the PPP is, if you took a loss (negative net income), you do not qualify. Horrible for first year business who 9/10 take a loss on their first year. I think this bill should be corrected for this reason. I’ve seen a lot of owners ruled ineligible due to this.

Richard, you are right. The PPP doesn’t help someone who only just started their business and so hasn’t yet ramped up to profitability–unless they employed W-2 workers.

I have a blog post coming out in a week about how Covid-19 closures kill small businesses. And the newest small businesses probably got hit hardest.

I need to know how I can apply I have a daycare center and I need help with money!!

If you’re a sole proprietor–and Congress restarts the program–you apply by filling out the application form as described here. Then you give that form to a bank.

And as noted in blog post, you may also be able to apply online through someone like PayPal, Kabbage, etc.

You didn’t mention if we have to pay that money back? Is it free for sole proprietor to apply for PPP loan without any restrictions?

If you do this right, it should be free money. More details here: https://evergreensmallbusiness.com/sole-proprietor-and-partnership-ppp-tax-rules/

1.) The loan amount requested is for one year, yes or no.

2.) What if a person started a business in February and because of the pandemic did not actually earn.

My question is could a person therefore project a annual salary. With or without employees.

Thanks in advance,

Maurice

In answer to first, question, no.

In answer to second question, I think you need either payroll or profits. So no payroll or profits, no PPP.

Sorry. I can tell from your question that this, unfortunately, does not work for a business owner in your situation. 🙁

That’s very nice of you to explain this for those who may be unclear. I’m a sole proprietor and missed the first release of the PPP by the time I really understood what I needed to do to apply.

I was very disappointed once I realized how simple it really was. Then I heard the PPP was available again. I checked my bank’s website and they were participating in the 2nd round ending August 8th.

My bank provided a liaison between myself and the SBA who assisted me with the application process to ensure everything was correct. I was approved on August 8th and I am very grateful.

So I think it’s a great idea to tell people to get prepared. Because if I hadn’t have been prepared with proper documentation, I might have missed the opportunity the 2nd time.

Thanks for caring and sharing.

What about LLC single members that started buisness in January of 2020 and do not not have a 1040c tax form as of yet?

Great question. You need to have been in business on February 15, 2020. For businesses without payroll in 2019 (or Schedule C owners compensation), the formula for first draw PPP loans looks at the first two months of 2020 and for second draw loans at the average payroll paid in 2020.

You can look at 2020. First draw loans should look at your profits in January and February. Second draw loans (assuming they become available) look at your 2020 earnings before you apply.

Note: This is an area (new businesses) where we’ll hopefully get some good additional info and instructions from SBA.

Thank you How kind of you to put this post.!

I am also a painter and wallpaper installer. . I did apply and did receive funds. However, , my first attempt through my large bank was not easy and not successful.

It was through a smaller bank referred by another small business owner that worked, easily.

And it has helped greatly. Especially because I’ve been unable to get any response from state unemployment.

Do this!

Sole Proprietor, I made under $1,500 in 2019 because of illness, I’ve filed my 2019 taxes. Should I apply?

If your Schedule C profit was $1500, your monthly earnings were $125. And that means your PPP loan would be $312.50 (or 2.5 times the $125).

BTW if there’s a second draw loan you can get because your revenues in 2020 are down 50 percent, you could also get another $312.50.

Those are the numbers. You’d need to decide whether they make sense to pursue.

Okay so I had a business as of February 15th as we had just did business XIV Valentine’s Day so being self-employed no business license however we were hoping to get a business going myself my mother and my daughter as we have been doing whole selling crafting different things and had decided to open a store now would we qualify for any of these programs if yes can you please leave a message or email me thank you very much for your time

Hi Shelly,

I removed your email address because otherwise you will get inundated with spam… as I do. But you maybe can get a PPP loan for the new business. As you note, you were in business on February 15, 2020. So you could get a “new business” loan based on the payroll for first two months. That might work. If your January and February average monthly profit was $4,000, for example, you should be able to get a $10,000 loan I think.

I think it is just wonderful that you are taking all this time to answer individual questions!!! I am a banker who did 85 of these loans earlier and now am in the midst of the forgiveness apps- lots of work but lots of good for clients and local businesses.

Great article, but there exist many different scenarios including my situation. My company invest in distressed real estate: buy at auction, fix and flip. I didn’t make money in 2019, I made purchases only. The auction is closed since March and I lost many opportunities. How and what programs apply to my situation. Many thanks.

It’s possible that your real estate activity doesn’t qualify as a “trade or business” which is what the PPP targets.

You’d need to be reporting your real estate activity on a Schedule C…

I heard kabbage.com has a new link for loan application…please can i get update about their new site to apply for loans ..?

I don’t really have a way to know which Internet address is right or most up-to-date… sorry. If a kabbage.com employee wants to post that info, though, I’ll make sure it’s visible.

they are not allowing the schedule C only. I know many who turned in a schedule c myself included. they want w2 or 1099 we all were denied. who ever wrote this should do a better job with what really happens to self employed people.

even the cares act isn’t accepting just a schedule c

The statement above is incorrect. The SBA lent money to hundreds of thousands of employee-less sole proprietors.

In fact, the very first question the SBA answers in its “How do I calculate the PPP Loan amount” document, available here, says this:

1. Question: I am self-employed and have no employees, how do I calculate my maximum PPP loan amount? (Note that PPP loan forgiveness amounts will depend, in part, on the total amount spent during the 24-week period following the first disbursement of the PPP loan.)

Answer: The following methodology should be used to calculate the maximum amount that can be borrowed if you are self-employed and have no employees, and your principal place of residence is in the United States, including if you are an independent contractor or operate a sole proprietorship (but not if you are a partner in a partnership):

• Step 1: Find your 2019 IRS Form 1040 Schedule C line 31 net profit amount (if you have not yet filed a 2019 return, fill it out and compute the value). If this amount is

over $100,000, reduce it to $100,000. If this amount is zero or less, you are not eligible for a PPP loan.

• Step 2: Calculate the average monthly net profit amount (divide the amount from Step 1 by 12).

• Step 3: Multiply the average monthly net profit amount from Step 2 by 2.5.

• Step 4: Add the outstanding amount of any Economic Injury Disaster Loan (EIDL) made between January 31, 2020 and April 3, 2020 that you seek to refinance, less the

amount of any advance under an EIDL COVID-19 loan (because it does not have to be repaid).

Your 2019 IRS Form 1040 Schedule C must be provided to substantiate the applied-for PPP loan amount. You must also provide a 2019 IRS Form 1099-MISC detailing

nonemployee compensation received (box 7), invoice, bank statement, or book of record establishing you were self-employed in 2019 and a 2020 invoice, bank statement, or book

of record establishing you were in operation on February 15, 2020.

I just want to say thank you to you writing such a good article and answering every single person’s comments. You’re doing a fantastic service considering how typically unclear the IRS usually is. I only wish I had a business last year as I was on disability and I’m just starting a business now in 2020

Hello,

My husband and I have a small IT company through our LLC. We don’t have any employees and just except payment as a pass through. We complete a form 1120 S for our business and form 1040 as a married couple. Our CPA says that we are not eligible for the PPP as we don’t pay payroll to employees. Would we be covered under the Sole Proprietor or Partnership applications?

The P in PPP stands for paychecks. And if you don’t have paychecks because you don’t “do” payroll then, yes, sorry, you can’t get a PPP loan.

My question wasn’t with whether I qualified for the PPP loan but the terms of it being forgiven. I’m a new business (sole proprietor w/no employees) that just started at the beginning of October 2019. I was able to submit an estimated 2020 Schedule C and received a loan that way. However, confused as to is the entire loan amount forgivable, if used however I want or does the 60% towards payroll and the rest toward rent apply?

OK, so you want to use the PPP loan to pay the proprietor (I.e., you.) That’ll give you forgiveness… and it is also means you won’t lose tax deductions. See this blog post: https://evergreensmallbusiness.com/sole-proprietor-and-partnership-ppp-tax-rules/

Hi, I’m confused. If the PPP is the those who don’t have employees then how would I have paychecks? How can I get help with the start up of my business which I started in June?

The proprietor (the owner) would need to write a check to her or himself. The forgiveness applications, in other words, require a payment or payments be made.

That looks like the range that I would be in

Good morning. I have two questions.

If you have a business entertainment

But the name wasn’t registered yet

Can you still apply? If something like

That happened, you applied and

You qualified, because you did not have

A business bank account yet and the money went to your personal bank

Account, do the bank have the right

To keep the money and send it back to SBA? PLEASE HELP AND THANK YOU

Not sure I understand what your questions are. But you should still be able to make a PPP loan work even if you don’t have a special business bank account. The one problem with having funky or jury-rigged banking and accounting, however, is you won’t easily be able to show stuff to the banker in a way that makes sense and that “looks” right.

Thank you so very much Stephen for all your help!

One question

How do I get a PPP number ?

I did get an SBA application number for a disaster loan, which got approved for a 30 year loan.

Is that the same number I have to use for the sole proprietor application PPP loan?

Thank you so very much!

Krishan

I think the SBA assigned the PPP number when the bank submits the loan to the SBA.

A little late for me, but still a good resource for other entrepreneurs! I’ll be sure to share this with my brother who’s starting his own business. Thanks for sharing!

Hello,

What about S Corps (Vs Schedule C) with the owner being the only employee? I use Quickbooks online. QB created a report showing how much PPP I was eligible for based on 2019 W-2 wages (did not include distributions). So are distribution excluded because there is no SE tax on these? Then it asked me to apply through QB Capital. I did and got rejected. A month or so later QB Capital told me I could apply again and I got rejected again. Both times they said I didn’t meet the minimum threshold for PPP loan in my state (GA)? So I asked for too little help? By the time I checked with my local bank (BAC) they had already cut off the application period. Also I did get EIDL of $1000. I heard you cannot get both? Is that accurate? Wondering if I should try a 3rd time.

S corporation payroll costs include W-2 wages paid to employees (both owner-employees and non-owner-employees), state and local payroll taxes, health insurance, and retirement benefits.

So the accounting requires a little more work… but other than that, the application works the same way. E.g., if the average monthly payroll cost (including all that stuff I just mentioned) equals $4,000, the loan equals $10,000.

BTW, there is no PPP minimum. And Georgia wouldn’t have (or shouldn’t have) a state law that rewrites federal law. I suppose it’s possible the bank decided some PPP loans are too small to bother with… that’s an ugly possibility. This earlier blog post may provide additional info that’s useful: https://evergreensmallbusiness.com/paycheck-protection-loan-formula-explained-and-illustrated/